Wired in Series

Malaysia booked equidistance as a parallel circuit. The IISS has now traced the wiring: one Taiwan break puts forty-one per cent of GDP through a single conductor.

Westports sits on the Malacca Strait with a container record set the year before the war — 11.3 million boxes in 2025 — and in June 2026 it is doing something stranger than booming: turning away diverted cargo with unclear final destinations to protect its yard, while the water it sits on has the best quarter of its commercial life for the worst possible reason.

The Strait of Hormuz has been effectively shut since 28 February — transits running at roughly six per cent of a pre-war cadence that topped a hundred ships a day, war-risk premia repriced from a fifth of one per cent of hull value to a full one per cent for seven days of cover, all twelve International Group P&I clubs having cancelled their war-risk extensions on seventy-two hours’ notice in the first week — and the crude and LNG that used to cross the Gulf now reroutes through the corridor Malaysia shares with Singapore, a waterway that already carried roughly a quarter of seaborne oil before anyone needed it to carry more.

Kuala Lumpur has played the moment the way it plays every moment: in late March the prime minister telephoned Iran’s president and by early April had walked seven Malaysian tankers through a closed strait on the strength of the call, thanked Tehran publicly, and has watched the national fuel assurance roll forward one month at a time since — to May, then end-June, then end-July, now ‘beyond July’ this week — cover renewed on a calendar, not secured on a structure.

A barrel changes hands in the high eighties — a two-month low printed this week, not because the war resolved but because Washington floated a weekend signature on a fourteen-point draft that would reopen the strait within thirty days, and neither the mines (six months to clear, on the American estimate) nor the war-risk architecture reprices on a draft — and Malaysia, net LNG exporter, premium-crude seller, friend of everyone, is still being paid, not punished, by a war it stayed out of.

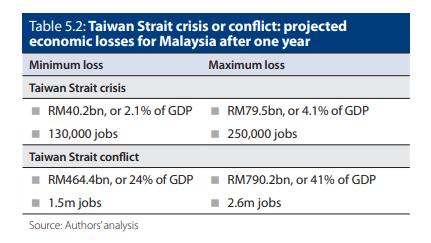

Its June report on a Taiwan Strait contingency prices what happens when the next chokepoint event is not someone else’s — when the strait that closes is not the one Malaysia profits from but the one its flagship industry is plugged into. The maximum estimate for a year-long conflict is RM790.2 billion, or US$172.6 billion: forty-one per cent of GDP, 2.6 million jobs.

The number is not the finding.

The finding is the wiring diagram underneath it — the demonstration that the equidistance Malaysia has treated as redundancy is nothing of the kind.

Not a parallel circuit. A series one.

Equidistance was drawn as a parallel circuit

The doctrine is explicit and it is proud.

The economic logic beneath the diplomacy runs like a parallel circuit: keep a heavy-gauge connection to China, the largest trading partner; keep a second to the United States, the largest single investor among the three principals at roughly RM7.6 billion of annual inbound FDI; keep a third to Taiwan, which took about RM67 billion of Malaysian exports in 2024. If one leg browns out — a tariff war, a sanctions round, a quarrel that is not Malaysia’s — current reroutes through the others and the lights stay on.

The 2025 tariff shock seemed to prove the design: Putrajaya diversified toward the EU, the Gulf and Africa within months, and growth ran above five per cent into the autumn.

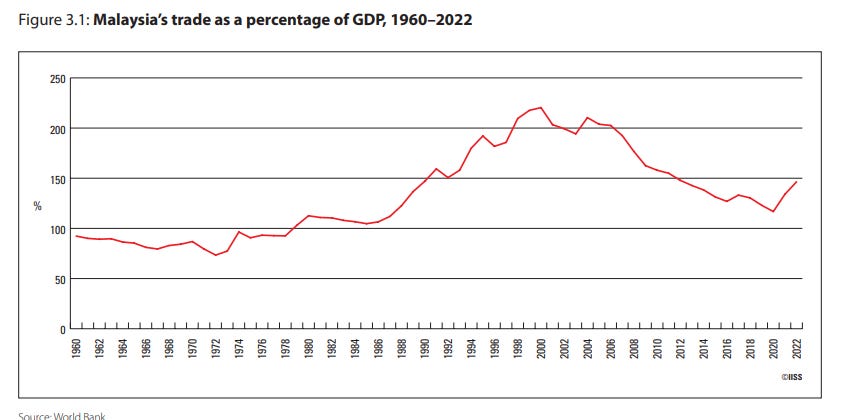

The load this circuit carries is enormous, which is precisely why the design matters. Malaysia’s trade ratio — exports plus imports against GDP — stood near a hundred and fifty per cent in 2022, down from its 2000 peak above two hundred but still among the highest of any mid-sized economy on earth.

A trade ratio of that size is a decision to run the national economy at high current all the time — to draw prosperity through the wires rather than generate it behind a wall — and the doctrine’s entire claim is that the wiring is redundant: many sources, many sinks, no single point of failure.

Read that claim as an electrician reads it, and one question decides everything — not how many wires run into the house, but whether they ever pass through the same junction.

The IISS report’s contribution is to have traced them.

They do.

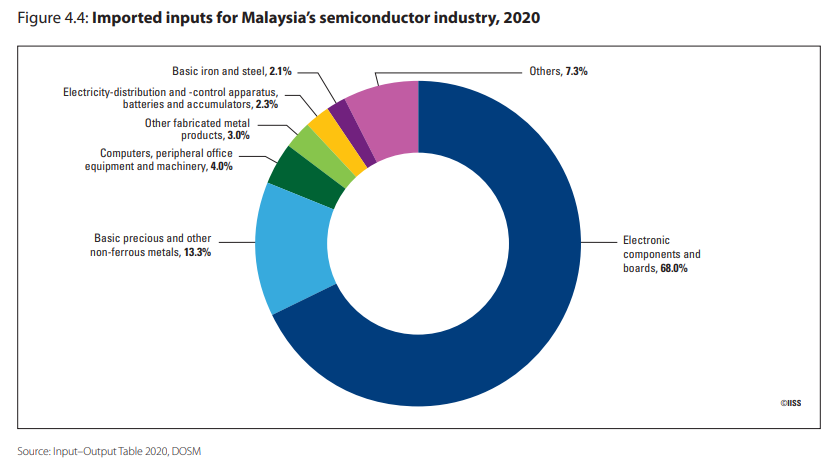

The board is one supplier deep

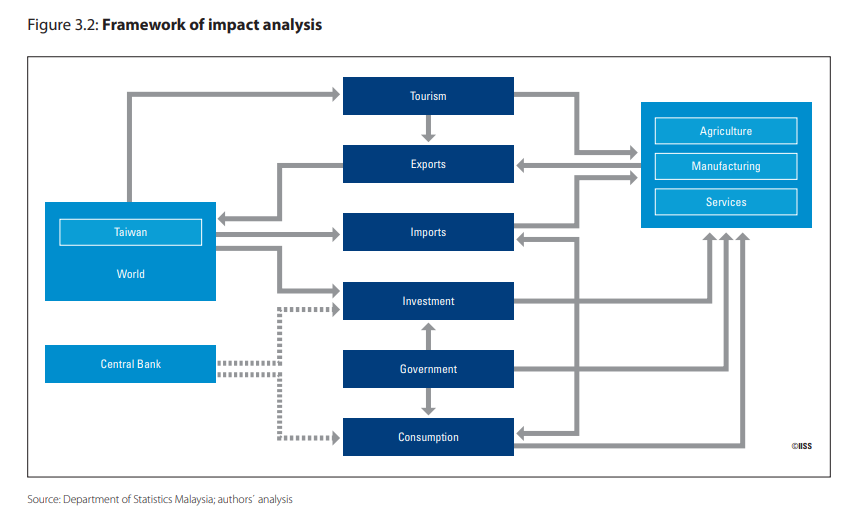

Start where the report starts, with the export ledger.

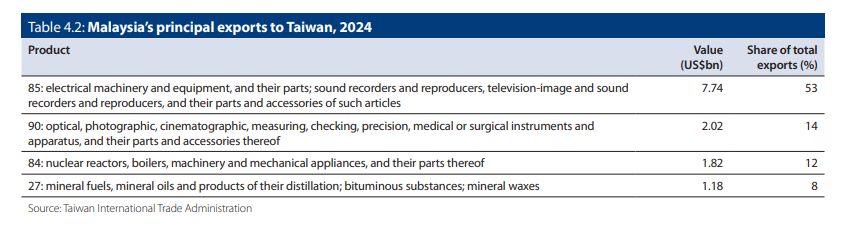

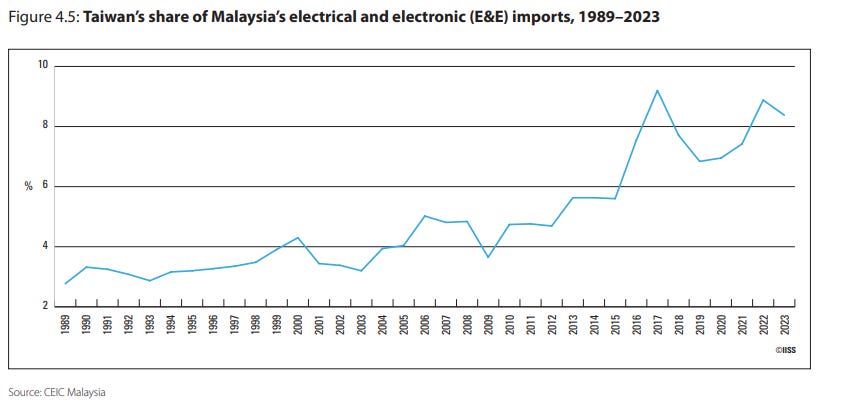

Electrical and electronic products are sixty-seven per cent of everything Malaysia sells to Taiwan.

But the export line is the shallow reading; the deep one is on the import side.

The report quantifies what a break at that node conducts.

Its econometric pass finds that halving E&E imports from Taiwan does not merely halve the matching exports back to Taiwan — a loss of RM32.6 billion — it cuts Malaysia’s E&E exports to every other destination by a further RM10.7 billion, because the products sold to third countries cannot be built without the inputs that stopped arriving.

That is the signature of series wiring: the fault does not stay in the leg where it occurs; it propagates through the whole board, dimming customers who have no quarrel with anyone.

Stockpiles soften the first weeks — firms learned inventory discipline in the pandemic and again in the tariff war — but those buffers were built for disruptions measured in months, and in a sector where the product itself goes obsolete on the shelf, a deep inventory is a depreciating asset, not a reserve.

This is the section of the report that should be read twice, because it converts a diplomatic abstraction into an engineering fact. Equidistance describes Malaysia’s relationships. It does not describe Malaysia’s circuit, and in a contingency it is the circuit, not the relationships, that carries the current.

Forty-one per cent is the fault current

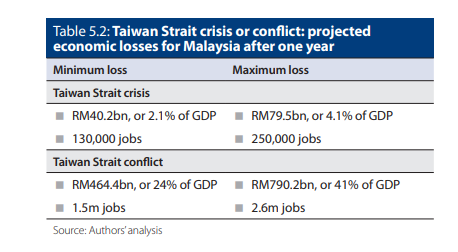

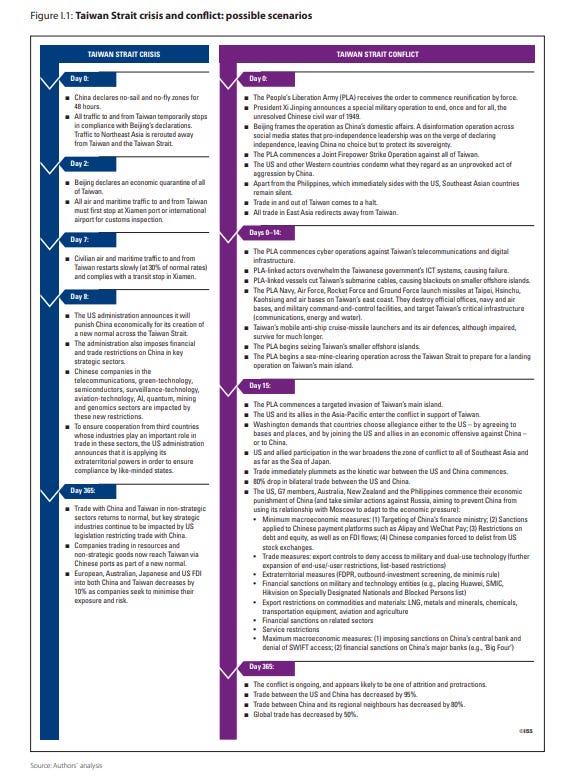

The report runs two scenarios across one year, each with a minimum and maximum case.

The crisis scenario — an air-and-sea quarantine of Taiwan, traffic recovering to half its prior level and staying there — costs Malaysia between RM40.2 billion and RM79.5 billion, between 2.1 and 4.1 per cent of GDP, with up to 250,000 jobs gone, concentrated in E&E and in a tourism sector that contributes fifteen per cent of GDP and would lose its Chinese segment, twelve per cent of receipts, overnight. Painful, and historically legible — the Asian financial crisis took 7.4 per cent of GDP in 1998, the pandemic 5.5 in 2020.

A quarantine is a shock Malaysia’s institutions have rehearsed.

The conflict scenario is not. A full invasion, US and allied entry on Day 15, bilateral US–China trade down ninety-five per cent by year-end and global trade down by as much as half — wartime numbers, calibrated against the fifty-five to sixty per cent collapse Glick and Taylor estimate for the whole of the Second World War — produces Malaysian losses of RM464.4 billion to RM790.2 billion: twenty-four to forty-one per cent of GDP, 1.5 to 2.6 million jobs on the report’s employment elasticity of 0.38 per point of output.

The estimate is deliberately maximalist — it models no counter-cyclical response from Putrajaya, because no honest model can predict one — but the calibration that matters sits in the report’s own historical mirror: Glick and Taylor put the cost of the world wars to neutral countries at 7.2 and 11.8 per cent of GDP. Malaysia, neutral, loses up to forty-one.

Hold those two figures against each other, because the gap between them is the article’s argument in a single comparison.

Twentieth-century neutrality cost a tenth of the economy at worst; twenty-first-century neutrality, for a country wired like Malaysia, costs four times that — more than many combatants surrendered in the wars themselves.

Nothing about the legal status changed.

What changed is the trade ratio — the decision to run at a hundred and fifty per cent — which acts on an external shock exactly as a conductor acts on current: it does not attenuate the fault, it transmits it at full amperage.

The fault current is not proportional to your distance from the short.

It is proportional to the gauge of your wire.

The loop held until Day 15

Here is where the mechanism turns reflexive, and it is worth building the loop in full because the report supplies every step without naming it.

The belief: equidistance insulates — staying close to both blocs protects Malaysia from their collision. The behaviour the belief licenses: deepen both legs simultaneously, because if connection is protection, more connection is more protection — and so Taiwan’s share of E&E imports rises in every period, Chinese FDI compounds, the report observes that most of the Malaysian public still treats a Taiwan contingency as an abstraction, and no structural mitigation is undertaken.

The altered fundamental: the deepening itself rewires the economy — every additional point of integration is another strand in the conductor, so the belief in insulation manufactures, year by year, the exposure it claims to be insulating against. And the feedback: each calm year, each crisis profitably skirted — the tariff shock absorbed, the Hormuz closure monetised, seven tankers talked through a war zone on one phone call — confirms the doctrine and licenses the next increment of integration.

The loop is self-reinforcing.

The perception is not measuring the system; it is building it.

The inflection — the moment the loop turns self-defeating — has a date in the report’s own scenario: Day 15, when Washington enters the war and demands that every country in the region choose allegiance, basing rights and sanctions participation included.

Equidistance is an option that pays only while unexercised; the contingency it was bought against is the very event that cancels it.

And the Hormuz war, run live since February, has already shown the retail version of that cancellation: Malaysia’s safe passage through a closed strait was not produced by the doctrine, it was produced by the prime minister personally, call by call, seven hulls at a time — protection as a favour renewed at the discretion of a belligerent, which is the opposite of insulation. The parallel circuit confirmed itself for twenty years because nobody ever threw the breaker.

The scenario throws it.

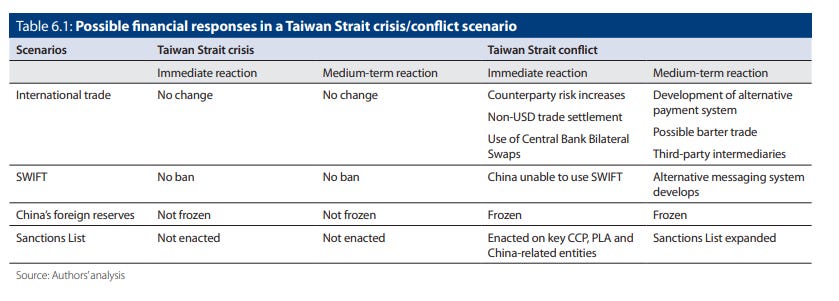

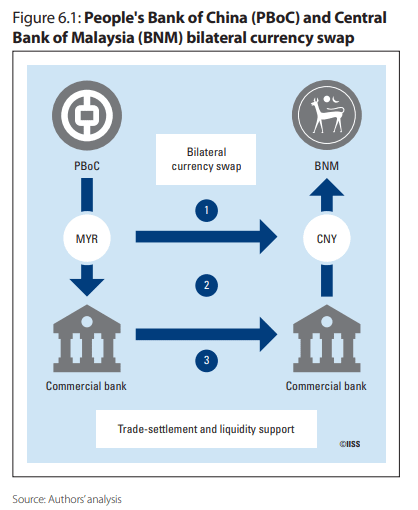

The swap line is not a fuse

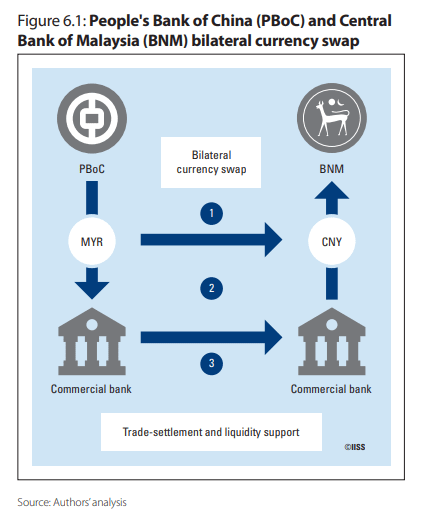

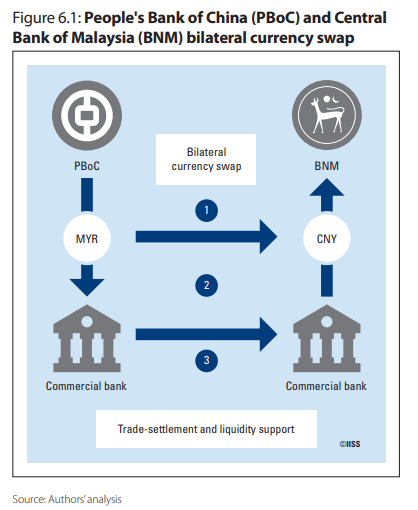

Even in the conflict scenario, China’s remaining US$652.3 billion of Treasuries — pared six per cent in March alone as Beijing trims exposure — makes the PBoC, in the report’s judgement, too large for the system to fail. And Malaysia holds what looks like a dedicated fuse: the bilateral PBoC–Bank Negara swap line, in place since 2009 and renewed in 2021, through which ringgit–renminbi settlement could route around a sanctioned dollar system entirely, on CIPS rails, the way Indian banks built rupee vostro accounts for Russian trade after 2022.

If the financial leg holds, the argument runs, the real-economy damage is survivable — Malaysia trades on through the side channel.

The report’s own second-order analysis melts the fuse.

A swap line is plumbing; what moves through plumbing is decided by compliance officers, and a Malaysian bank facing US secondary-sanctions exposure will restrict renminbi settlement not because the channel is blocked but because using it endangers every dollar relationship the bank owns — the correspondent accounts, the letter-of-credit confirmations, the clearing access that carries Malaysia’s palm oil, LNG and refined-product exports through USD-based commodity houses. The fuse fails for the same reason the circuit fails: the dollar leg and the renminbi leg are not independent, because the institutions that would operate the alternative are themselves wired into the system the alternative is meant to bypass. De-risking is the financial sector’s series wiring.

The report expects letter-of-credit non-confirmation, settlement lag, counterparty premia and a working-capital squeeze on export SMEs — the fault current, again, arriving through the very channel built to interrupt it.

The reading on the meter

Assemble the whole board and the report’s deepest finding is not the forty-one per cent — it is that the cost of someone else’s war now scales with openness rather than with proximity or participation, which means the most globalised neutrals carry more war exposure than some combatants did a century ago, and carry it unmarked, because nothing in a trade ratio looks like a munition.

Malaysia’s number is Malaysia’s, but the wiring is the region’s: every economy that read integration as insurance has been running the same loop, and the IISS has simply been first to put a meter on one of them.

My verdict is that equidistance is a real diplomatic asset and a non-existent economic one, and Malaysia has spent two decades paying premiums in the first currency against a peril denominated in the second.

The doctrine buys voice, optionality, the seven-tanker phone call — genuine goods. It does not buy a single ohm of resistance between Hsinchu and Penang, and the report’s service is to have separated the two ledgers that ‘active non-alignment’ had allowed to blur into one.

The playout starts on the desks that already moved once.

When the 2025 tariffs landed, Malaysian Pacific Industries fell twenty-three per cent in the wake of one announcement — the calibration print for what Bursa Malaysia’s semiconductor complex does when the Taiwan node so much as flickers, and in a conflict the report expects that repricing to be deep and durable rather than sharp and mean-reverting.

The tariff print itself has already round-tripped — the stock trades within sight of its fifty-two-week high this week, the loss unlearned inside a year — which is not a rebuttal of the calibration but the loop in miniature: every repricing that reverses teaches the market to treat the next flicker as an entry, right up to the one that is not.

The structural implication lands in the energy market through the corridor itself: the Hormuz closure has already shown — as I argued during that war — that the insurance market shuts a strait before the first missile does, and the same architecture of war-risk premia, P&I withdrawal and sovereign backstops would migrate east to the Malacca–Singapore lane in any Taiwan contingency, putting a standing risk premium into delivered LNG costs for North Asia and repricing the option value of every storage and transhipment asset on the strait — including the Maharani Energy Gateway in Johor, whose free-zone gazettement decision is due from Kuala Lumpur before the end of 2026 and which is, in effect, a levered bet that chokepoint risk is now a permanent feature of Asian freight.

Two gauges will tell whether the loop is still running.

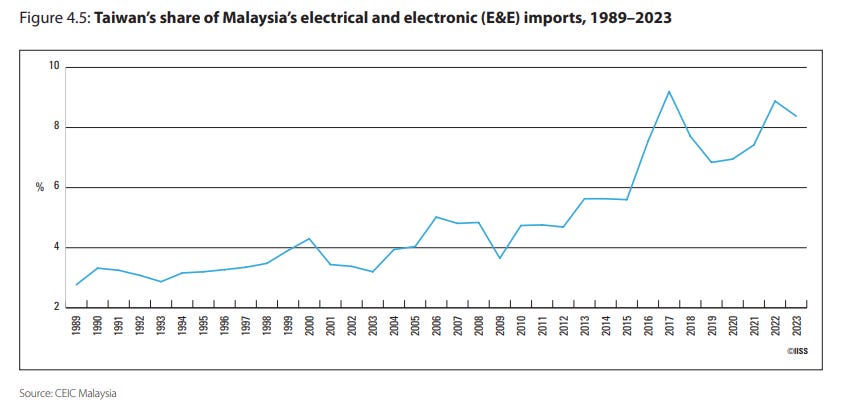

The first is Taiwan’s share of Malaysia’s E&E imports: 8.5 per cent at the 2022 reading, rising for three decades — if the doctrine were genuinely converting into structure, the 2026 print would fall; the thesis here says it rises, because the loop rewards deepening right up to the inflection.

The second is the report’s own early-warning indicator: sustained PBoC non-subscription to new Treasury issuance — holdings dropping decisively below US$600 billion in the monthly TIC data — the next print, covering April, lands on 18 June — would mark Beijing repositioning for the scenario in which the wiring is finally tested.

The corridor is being paid wartime economics this quarter — bunkering, transhipment, the war-risk premium embedded in every delivered cargo — by a war Malaysia neither joined nor priced, even as the flagship terminal at Port Klang turns away the boxes that same war diverts toward it.

America’s strategic ambiguity about Taiwan makes it very difficult to determine what would happen if China attempted to invade Taiwan and block the Malacca Strait. However, America’s attack on Iran and its expenditure of interceptors in the Middle East makes a Chinese attempt on Taiwan more likely than before. It will be interesting to see how countries re-align if the Hormuz Strait re-opens and it will be interesting to see how countries re-align if conflict between China and Taiwan increases. The fog of war is real and the proxy battles between the US and China are forcing some difficult decisions for everyone.

Interesting analogy. I think any attempt to disrupt the Malacca strait leads to WWIII and the “taking of sides” would be irrelevant. It’s like playing the game of tic-tac-toe.