What Could Possibly Go Wrong? Ryanair's Turkish Equation

Why being cheapest doesn't matter when currencies collapse and governments pick winners

“In theory, there is no difference between theory and practice. In practice, there is.” — Yogi Berra

Analyzing Ryanair’s potential expansion into Turkey during my studies was a standout project. It combined my experience in Turkey, my European education, and a direct look at how government policy shapes corporate strategy.

Looking back from January 2026, the key takeaway is that airline markets are driven by more than competition, and both the industry and my understanding of it have shifted dramatically.

In 2023, Turkey looked like a textbook target for Ryanair’s expansion.

The Aviation Price Index of $28.51 per 60 kilometers signaled both demand and room for low-cost disruption.

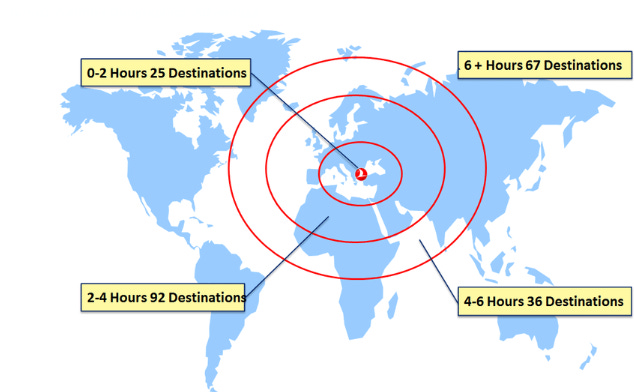

Istanbul Airport had become one of only three global hubs with over 300 destinations, rivaling Frankfurt and Paris. With 85 million people, a median age of 32, a growing middle class, a massive European diaspora, and 50 million tourists annually, the market seemed perfect for Ryanair’s model. Yet the airline only operated seasonal routes to Bodrum and Dalaman. This limited presence, so different from its comprehensive European network, suggested something deeper was blocking entry.

The research revealed what spreadsheets miss:

Ryanair wouldn’t just be competing with other airlines in Turkey—it would be confronting nation-state industrial policy. Turkish Airlines functions as strategic infrastructure.

The government uses aviation to position Turkey as a Eurasian bridge, project influence across the Middle East and Africa, and demonstrate national achievement. Istanbul Airport wasn’t built as a commercial facility that happens to serve Turkish Airlines; it was designed explicitly as the flag carrier’s fortress hub, with the airline controlling over 50% of slots through coordinated state-commercial strategy rather than market competition.

Living in Turkey and studying in Europe gave me perspective on dynamics that pure economic analysis misses.

When Turkish people discuss Turkish Airlines, there’s this blend of national pride and practical frustration—proud of the airline’s global reach, annoyed at domestic fares that contradict low-cost rhetoric. Political sensitivities around aviation policy, informal advantages from government relationships, bureaucratic processes that favor or hinder entrants—these weren’t theoretical concepts but lived realities I’d observed.

Porter’s Five Forces analysis revealed structural barriers beneath the surface attractiveness. Turkish consumers are price-sensitive, show minimal brand loyalty, and switch airlines effortlessly—factors that usually favor low-cost carriers. But airport slot access creates massive constraints. Ryanair’s European model depends on secondary airports with weak bargaining power, desperate for traffic. That option doesn’t exist in Istanbul.

The main airport is slot-constrained and dominated by Turkish Airlines. Sabiha Gökçen offers lower costs but lacks connectivity and prestige to attract premium traffic.

Competitive rivalry analysis was particularly revealing.

Turkish Airlines competes across all segments with particular strength in premium and connecting traffic. Pegasus Airlines has established low-cost presence domestically and on select European routes. Most tellingly, Turkish Airlines created OnurAir as a low-cost subsidiary, though it has struggled operationally and continues to face persistent customer complaints. This demonstrates Turkish Airlines’ awareness of market segmentation and determination to defend the low-cost segment, even if execution has been problematic. Any Ryanair entry would trigger aggressive price competition, compressing already thin margins industry-wide.

Currency volatility proved a risk I initially underestimated.

The Turkish lira’s swings against the euro create brutal pricing challenges. Fares must stay competitive in lira for Turkish customers while generating adequate euro returns for a European carrier. Meanwhile, major costs—aircraft leases, fuel, maintenance—are dollar or euro-denominated. When the lira depreciated sharply multiple times between 2021 and 2025, this mismatch destroyed profitability instantly, regardless of operational efficiency.

Substitution threats vary significantly by segment. Domestic routes under 500 kilometers now face real competition from Turkey’s expanding high-speed rail network, which has captured substantial market share on routes like Istanbul-Ankara. For international routes to neighboring countries, bus services attract price-sensitive migrants despite much longer journey times. However, for most Western European destinations, air travel’s time advantage makes substitution unlikely unless fares reach levels rendering operations unprofitable.

Social and demographic analysis confirmed Turkish consumers match Ryanair’s target market in many ways. Younger demographics trade service for savings, digital literacy supports online booking, extended family networks drive domestic travel. But Turkish travel patterns differ crucially from Western European norms.

Religious and cultural events like Ramadan and Eid al-Adha create concentrated peak demand challenging capacity management models built for even distribution. This seasonality, combined with coastal tourism peaks, makes maintaining year-round high load factors difficult for models depending on consistent utilization.

Beyond Turkey-specific challenges, environmental regulation has emerged as perhaps the most significant threat facing the entire low-cost carrier model.

When I conducted the original analysis in 2023, environmental costs were emerging but manageable. By January 2026, the situation has intensified dramatically. EU ETS carbon pricing reached approximately 80 euros per ton by late 2025. National environmental taxes averaging 5-15 euros per passenger have proliferated across Europe. Analysts project these combined costs could increase another 30-50% by 2030.

These regulatory changes hit low-cost carriers disproportionately hard.

A 10-euro environmental tax represents vastly different percentages of a 30-euro Ryanair fare versus a 300-euro business class ticket. Ryanair operates on 3-5% margins compared to 8-12% for legacy carriers—there’s simply less capacity to absorb new costs. Worse, exemptions for transfer passengers favor hub carriers with connecting networks while disadvantaging point-to-point operators like Ryanair. This creates structural challenges for the low-cost model that operational efficiency alone cannot overcome.

Ryanair has responded through fleet modernization, ordering Boeing 737 MAX aircraft offering 15-20% better fuel efficiency. These investments genuinely reduce fuel consumption and emissions per passenger-kilometer. But whether incremental efficiency gains offset rising regulatory costs remains uncertain. If carbon costs continue rising, the economics enabling 20-30 euro fares may simply collapse. Unlike legacy carriers with business class revenue cushions, Ryanair depends on volume at thin margins that environmental policy increasingly compresses.

My original recommendations for Turkish market entry emphasized securing cost-effective slots at Sabiha Gökçen rather than competing for Istanbul Airport allocations, achieving 25-minute turnarounds, maintaining standardized 737 fleet operations, and relentless cost control. These operational elements remain essential. But reflecting from 2026, I’d add critical dimensions initially underemphasized.

First, partnership exploration with Turkish Airlines deserves serious consideration despite apparent business model incompatibility.

Feed agreements where Ryanair brings European passengers to Istanbul for connection onto Turkish Airlines’ intercontinental network could create mutual value. Ryanair gains Istanbul access and Turkish traffic. Turkish Airlines boosts long-haul load factors without cannibalizing European premium revenues. Cultural and operational integration would be challenging—coordinating scheduling, revenue sharing, and service standards between fundamentally different carriers. But the strategic logic is compelling enough to explore seriously.

More fundamentally, successful Turkish strategy requires political and regulatory navigation beyond operational execution.

Building relationships with aviation authorities, positioning as complementary to national interests, demonstrating commitment to local employment and economic development—these stakeholder management imperatives matter as much as cost control. This demands patience with bureaucratic processes favoring incumbents, acceptance of seemingly inefficient regulatory requirements, and willingness to operate subscale initially while building legitimacy. These capabilities differ fundamentally from the rapid scaling and ruthless efficiency driving low-cost carrier success in deregulated Western markets.

The project offered lessons extending far beyond Turkish aviation.

I started believing airline competition as mainly a function of operational efficiency and pricing. However, the analysis shows that institutional context, including government policy, regulatory frameworks, political relationships, and cultural factors, is just as important in shaping competitive dynamics as cost structures. Markets that look attractive based on demographics and economics can be out of reach if institutional barriers protect incumbents. To succeed, it is essential to align capabilities with the specific context and to recognize when structural factors make profitable entry impossible, no matter how strong the operational performance.

It also taught humility about business model transferability.

Ryanair’s model revolutionized European aviation and generated enormous shareholder and consumer value. But success reflected not just superior execution but favorable institutional contexts—deregulated markets, available secondary airports, weak incumbent responses, regulatory frameworks enabling aggressive cost optimization. Assuming seamless transfer to different institutional settings proved naive. Competing with government-backed carriers in markets where aviation serves strategic national objectives presents fundamentally different challenges than competing in open commercial markets.

What strikes me most is how this project—seemingly about whether one airline should enter one market—actually illuminated tensions defining contemporary global business.

There is a clear tension between private sector efficiency and public policy objectives. Economic rationality often comes into conflict with government strategic priorities.

Another key tension is between market competition and state strategy. Commercial logic can be at odds with industrial policies that are designed to serve national objectives.

A further tension exists between business model innovation and environmental sustainability. Innovations that generate consumer surplus can also create externalities, which regulation is increasingly requiring companies to address.

These tensions won’t resolve easily.

They characterize not just aviation but multiple industries where globalization, environmental imperatives, and nationalism create competing pressures.

Takes Off – Ryanair's Corporate Website")

Understanding them requires moving beyond traditional strategic frameworks to incorporate political economy, institutional analysis, and recognition that markets are embedded in social and political contexts shaping what’s possible regardless of operational capabilities. This evolution in my thinking—from viewing strategy primarily as competitive advantage and execution to understanding sustainable success requires navigating complex institutional environments where economic logic proves necessary but insufficient—represents the project’s most valuable lesson.

The Turkish case ultimately taught me that asking “should Ryanair enter this market?” misframes the question.

Better framing asks: under what conditions could market entry prove sustainable, what capabilities beyond cost leadership would success require, and do those conditions and capabilities align sufficiently to justify the attempt?

Success would depend on political navigation, regulatory patience, stakeholder management, and cultural adaptation—capabilities outside Ryanair’s core strengths. Whether developing these capabilities or partnering with entities possessing them justifies opportunity costs compared to deepening presence in familiar markets becomes a strategic choice without obvious right answer.

The ambiguity in this case was instructive. Business education typically uses case studies with clear strategies, but real-world situations are rarely that straightforward. The analysis indicated that market entry could succeed under certain conditions, though these may not always be achievable.

Uncertainty often limits decision-making. Recognizing the limits of analysis and learning to work with ambiguity were key lessons from this project. It provided more insight into how the world operates than any textbook.

A good but technical analysis.

Last summer we flew from GRU to IST and return. We flew on Turkish Airlines because it was the only direct flight. GRU to IST is a seriously long way, for those geographically challenged. There was no way we were going to waste another several hours changing planes in one or two European cities.

Then, we found Turkish Airlines to be extremely comfortable and refined. I'm a seasoned international travelor and I was genuinely impressed.

Then, IST is very modern, it sparkles. The walks can be a bit long but not so bad as GRU. IST prides itself on being the center of the world, and once you get there you will understand what they are saying. We saw more tourists in Istanbul than Paris, London or Washington DC. And Turkish Airlines takes great pride as serving more foreign countries than any other airlines in the world.

There is no way they will let some remote island like Ireland compete with them.

I hope you got to go there and see for yourself as part of your research for this article.