Watch Who They Attack

The data traveled from Richmond to New York to Yale — and at every stop, Washington shot the messenger.

"Who controls the past controls the future. Who controls the present controls the past." — George Orwell

I was halfway through my afternoon coffee, scrolling through the FT, when the pattern clicked.

It wasn’t the tariff data itself; I’d been tracking that for months.

It was the reaction.

Another government official publicly eviscerating another group of researchers for publishing findings that were, by any honest reading, careful, well-sourced, and entirely consistent with mainstream economics.

The New York Fed, Yale’s Budget Lab, Goldman’s chief economist, Deutsche Bank’s FX strategist — one by one, anyone who put a number on the cost of tariffs was being publicly criticized.

I put down the coffee and started pulling threads.

What follows is the product of that day — a research diary of sorts.

It’s what I read, what I thought, and the connections I made as the pieces fell into place.

I don’t have the pedigree of a Fed economist or the resources of Yale’s Budget Lab. But I’ve managed money long enough to know when the data is telling you one thing and the people in power are desperate for you to believe another.

This isn’t a polished research note.

It’s closer to how I actually think: messy, opinionated, and always coming back to the same question — what does this mean for how I position myself?

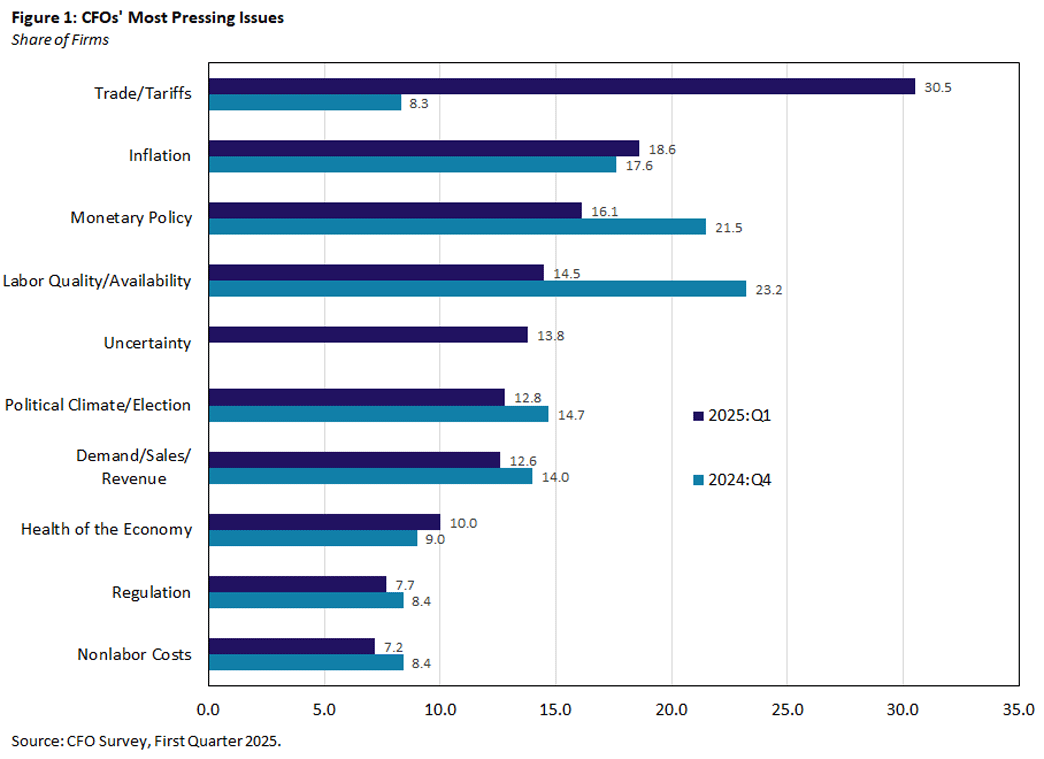

Back in April 2025, the Richmond Fed published one of the earliest rigorous assessments of the new tariff regime. Their conclusion was measured and cautious: tariffs could raise input costs, disrupt supply chains, and push up consumer prices — potentially outweighing any employment gains in protected industries. Nobody attacked the paper. It was hypothetical, forward-looking, and easy to dismiss as academic speculation.

But it established a baseline that every subsequent study would confirm: the cost of tariffs flows overwhelmingly downstream to domestic consumers and firms, not back upstream to foreign exporters. Empirical research has consistently found pass-through rates near 100%, and the Richmond Fed’s CFO Survey data reinforced this — businesses were already flagging cost pressures before most tariffs had even fully kicked in.

That was the warning shot. The real fireworks came when the data turned from hypothetical to actual.

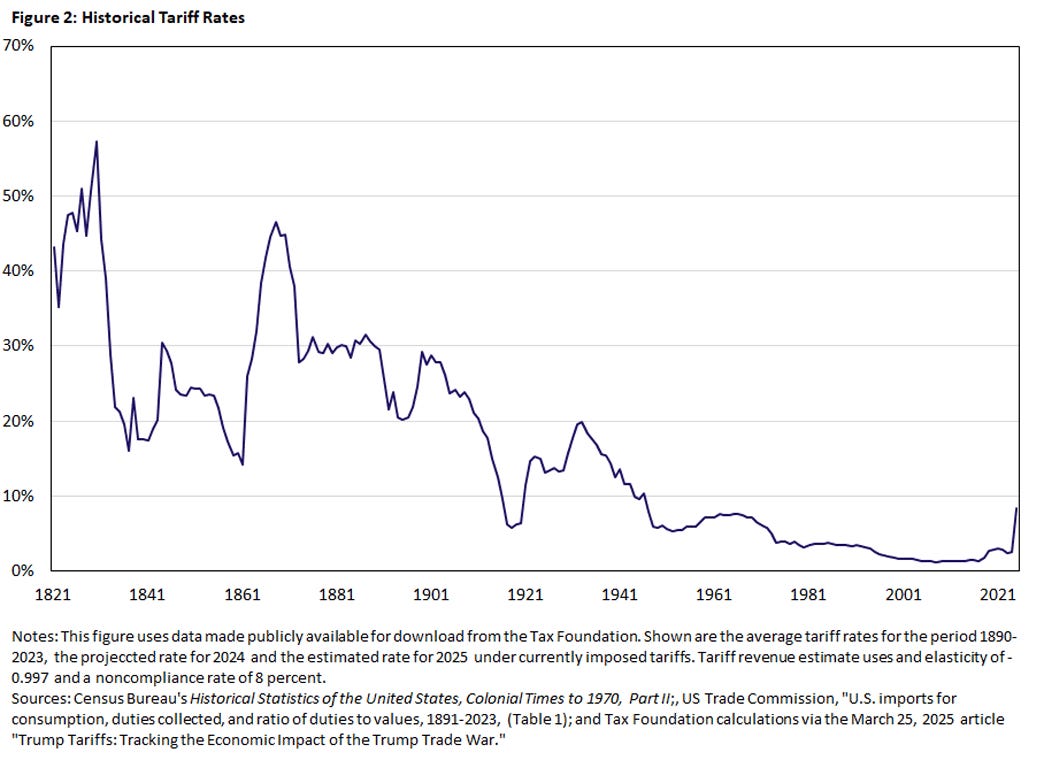

For context, U.S. effective tariff rates hadn’t been above 10% since the early 20th century. This regime is a structural break, not just a policy tweak.

The New York Fed Names the Number — and Gets Torched

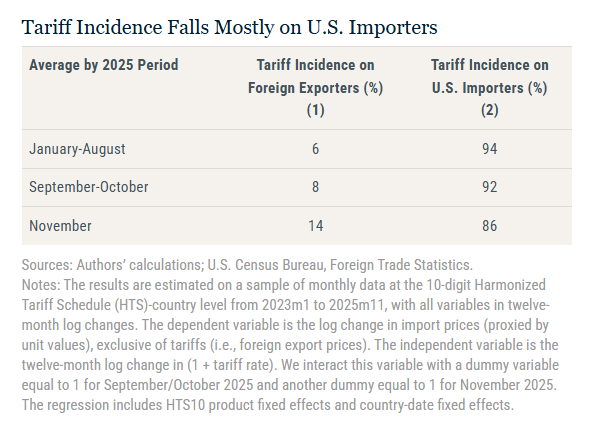

Estimating the real impact of the 2025 tariff regime was always tricky. Rates changed constantly, exemptions appeared and disappeared, and a single Truth Social post could change everything overnight. But the New York Fed gave it a serious try, and their findings were clear:

94% of the tariff burden fell on the United States during the first eight months of 2025. A 10% tariff produced only a 0.6 percentage point decline in foreign export prices — meaning virtually the entire cost landed on American importers, businesses, and consumers.

By November, pass-through had modestly improved to 86%, likely because foreign exporters were cutting margins to hold onto U.S. market share rather than any structural shift in who bears the cost. With the average tariff at 13% in December, the math was simple: U.S. import prices for tariffed goods rose roughly 11% more than non-tariffed goods.

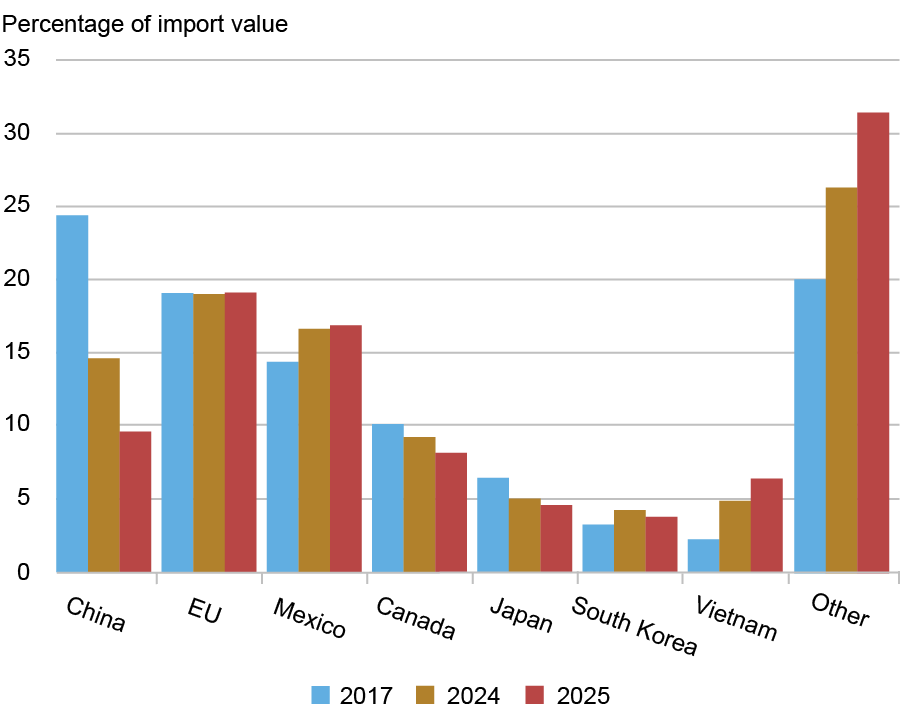

The data also revealed something structural.

Importers pivoted aggressively away from Chinese goods, with Mexico and Vietnam filling the gap.

But here’s the question no one in Washington wants to answer: how much of what’s labeled “Vietnamese” is actually Chinese product rerouted through a third country?

If the answer is “a lot,” and multiple investigations suggest it is, then the supply chain reshuffling isn’t diversification. It’s costly camouflage.

The 11% price premium on tariffed goods is hitting margins across the board in import-heavy sectors, and it isn’t temporary. Companies rerouting supply chains through Southeast Asia face new logistics costs, quality risks, and potential regulatory exposure if transshipment investigations intensify.

What the New York Fed is showing is textbook trade theory in action. In a typical partial equilibrium framework, a small open economy that imposes tariffs bears the full cost because it doesn’t have the market power to change the terms of trade.

The U.S. is not a small economy, but at 94% domestic incidence, it's behaving like one — which tells you something about the elasticity of foreign export supply in these product categories. Foreign producers have enough alternative markets, or enough margin flexibility, that they simply aren't cutting prices to absorb American tariffs.

The theoretical exception — a large country using "optimal tariff" logic to extract rents from foreign producers — requires a level of market power that the data says the U.S. doesn't have in most tariffed goods categories.

That’s the difference between what policy says and what the economic reality shows.

Then Came the Backlash

Kevin Hassett, Director of the National Economic Council, didn’t mince words on CNBC:

“It’s I think the worst paper I’ve ever seen in the history of the Federal Reserve system. The people associated with this paper should presumably be disciplined. What they’ve done is they’ve put out a conclusion which has created a lot of news that’s highly partisan based on analysis that wouldn’t be accepted in a first semester economics class.”

No counter-analysis, no alternative data—just a call for professional punishment.

This isn’t new.

Timothy Geithner warned S&P that a U.S. credit downgrade would be met with consequences. Trump reportedly told Goldman Sachs to fire Jan Hatzius — ironically, one of the more optimistic economists on Wall Street. Scott Bessent went after Deutsche Bank’s chief FX strategist George Saravelos.

The message is consistent and deliberate: publish inconvenient findings, and we’ll come after your career.

In a country built on free inquiry, that should alarm everyone, not just economists.

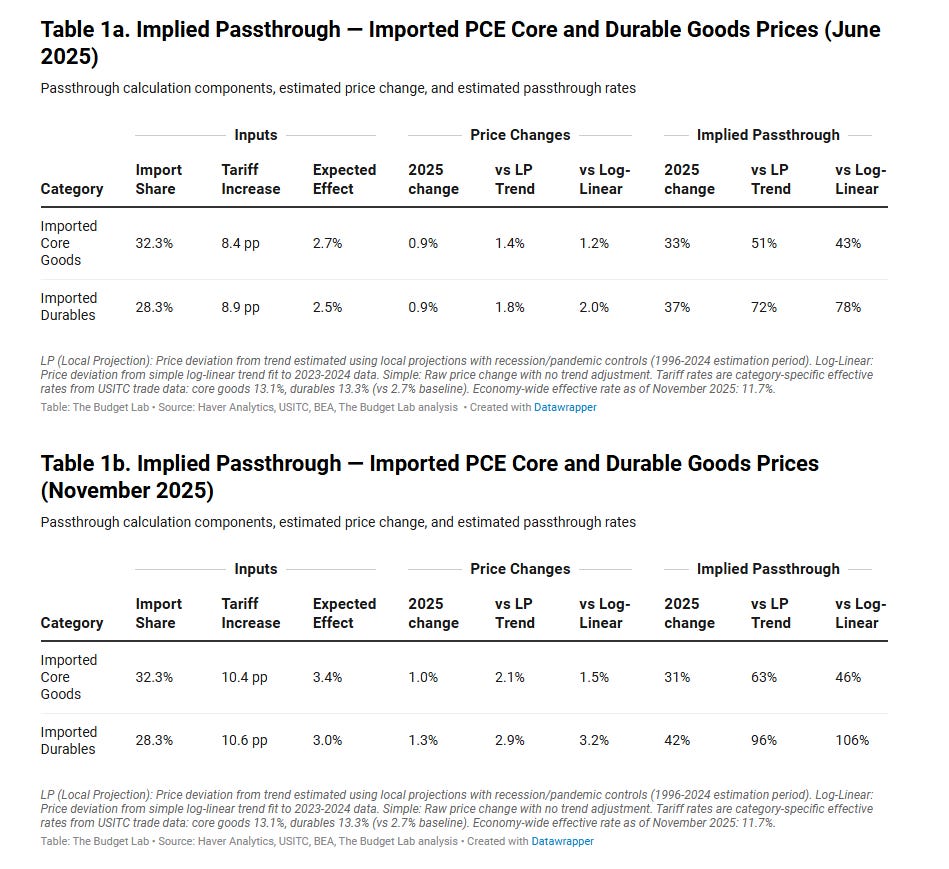

Yale's Budget Lab Steps Into the Crosshairs

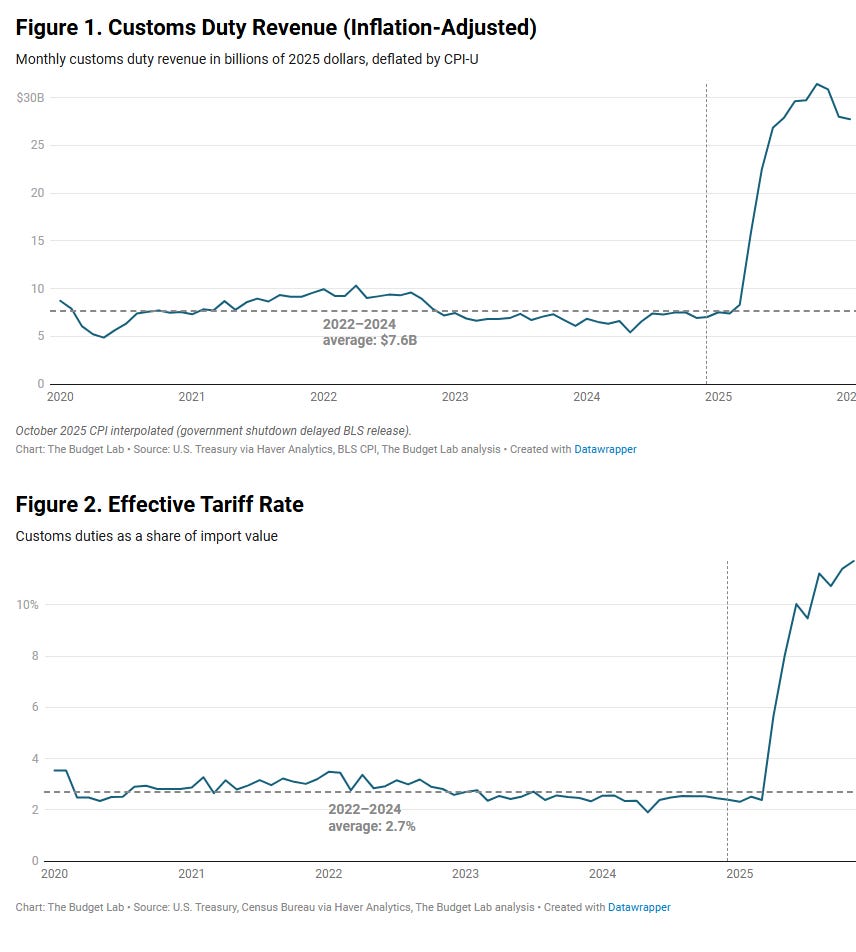

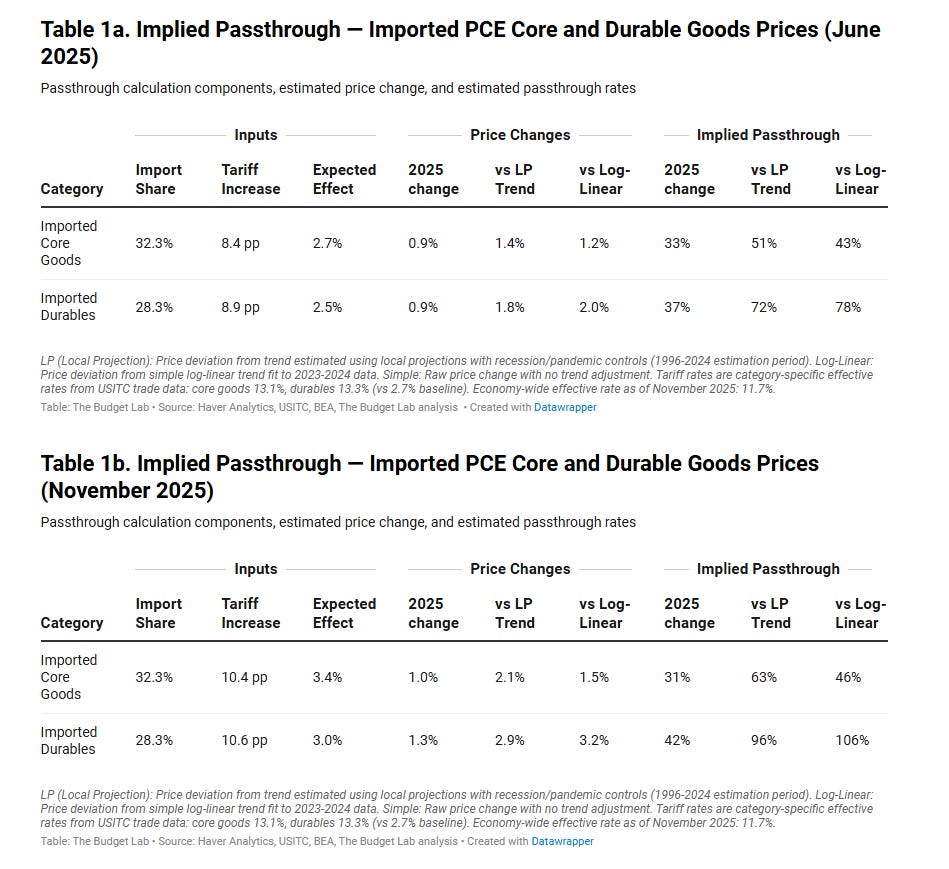

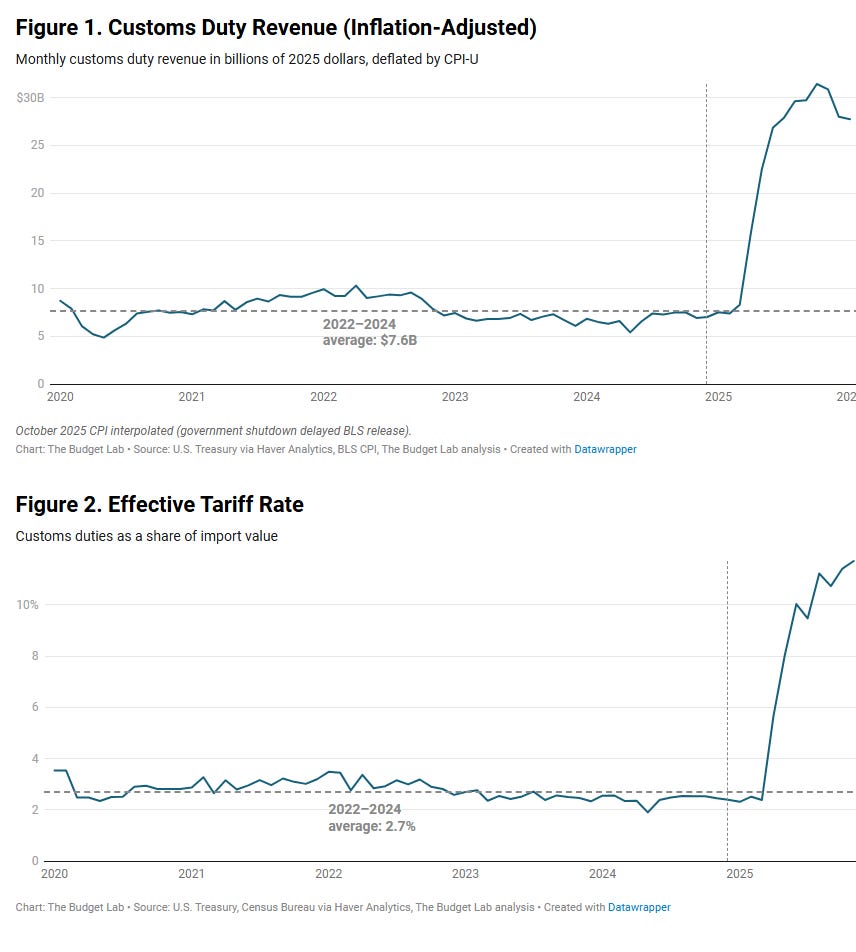

The headline numbers: $194.8 billion in inflation-adjusted customs revenue above the 2022–2024 average through January 2026, with the effective tariff rate reaching 11.7% in November 2025. Imported core goods and durable goods prices rose 1.0% and 1.3% respectively through November — both well above prior-year comparisons.

But the signal is in the divergence.

Core goods pass-through came in at 31–63%, depending on methodology. The range itself is informative — it reflects the difference between competitive and concentrated retail markets.

In highly competitive consumer goods categories, firms face a prisoner's dilemma: the first to raise prices loses market share, so everyone absorbs margin pain simultaneously. That suppresses measured pass-through in the short run, but it's inherently unsustainable.

Margins can only compress so far before firms either pass costs through or exit. What the 31–63% range is really telling us is that we're in the absorption phase, and the repricing phase is still ahead.

Durables pass-through ranged from 42–96%. That’s the canary. Durable goods manufacturers have far less room to absorb costs, and the data shows consumers were already front-running purchases — the $51 billion import surge through March 2025 was textbook anticipatory buying.

The question that matters for H2 2026 is: what happens when the pre-tariff inventory runs out? The cumulative import gap is still positive but shrinking fast. Once firms burn through stockpiled goods bought at pre-tariff prices, the pricing environment gets materially harder.

And the conventional hedge has completely broken down.

The most likely explanation is that capital account effects are dominating: declining confidence in U.S. institutional credibility and policy predictability is driving capital outflows that overwhelm any current account improvement from reduced imports.

For import-heavy companies, this means a double hit: higher tariff costs and unfavorable FX translation, with no offset in sight.

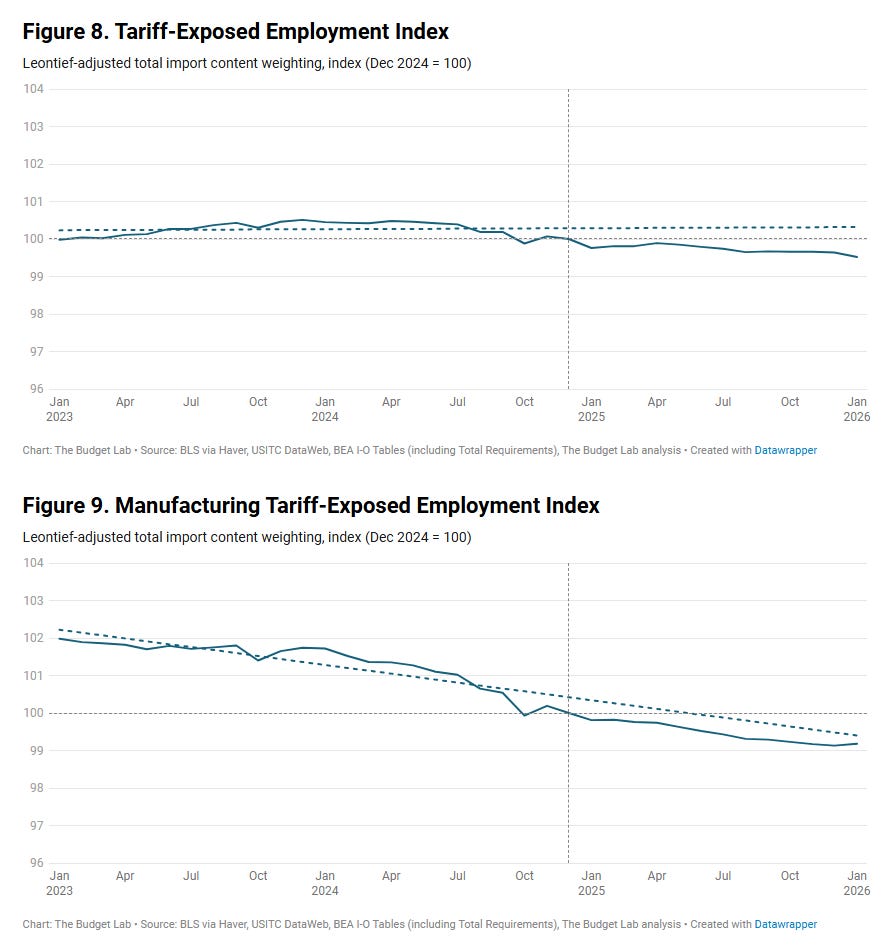

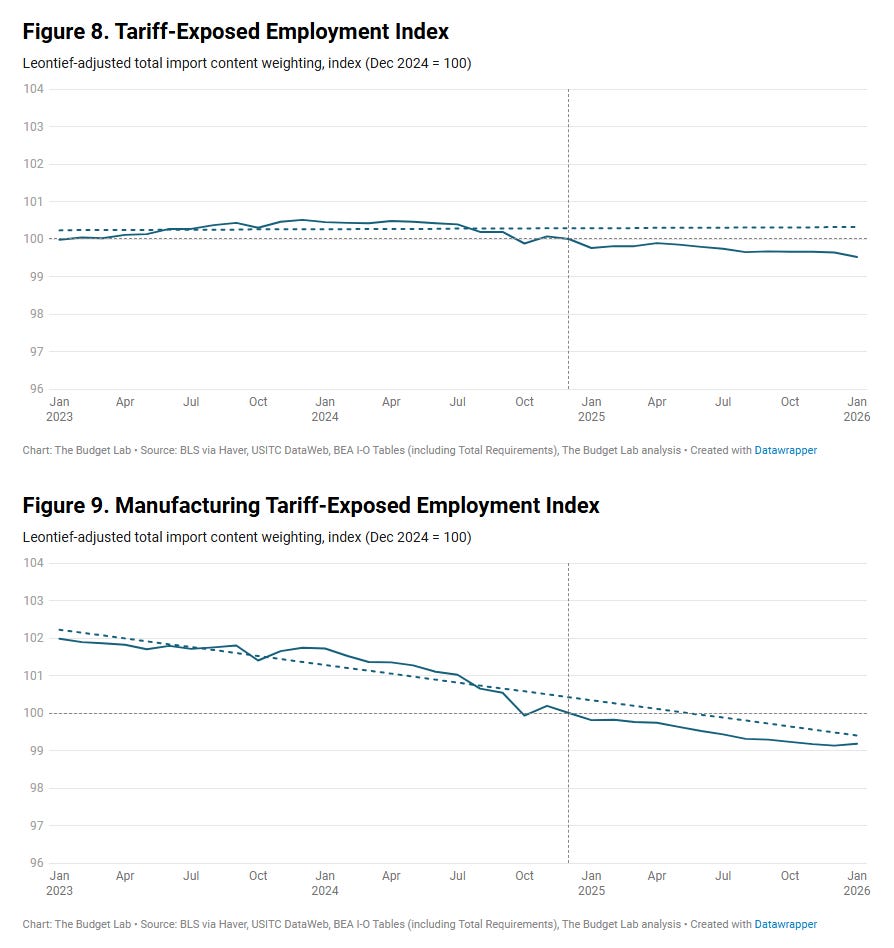

The employment picture offers a false sense of comfort. Yale found no definitive aggregate labor market effect, but the tariff-exposed employment index shows a 0.8% miss versus pre-2025 trend. That’s early-stage. If it accelerates — and the inventory depletion dynamic suggests it will — consumer spending takes the next leg down, and the “soft landing” narrative faces a serious stress test.

Underweight import-heavy durables and retailers that haven’t yet repriced for full pass-through. Watch for the inventory depletion inflection — when pre-tariff stockpiles run dry, you’ll see a step-change in pricing pressure that the market hasn’t fully discounted. The FX setup makes this worse, not better.

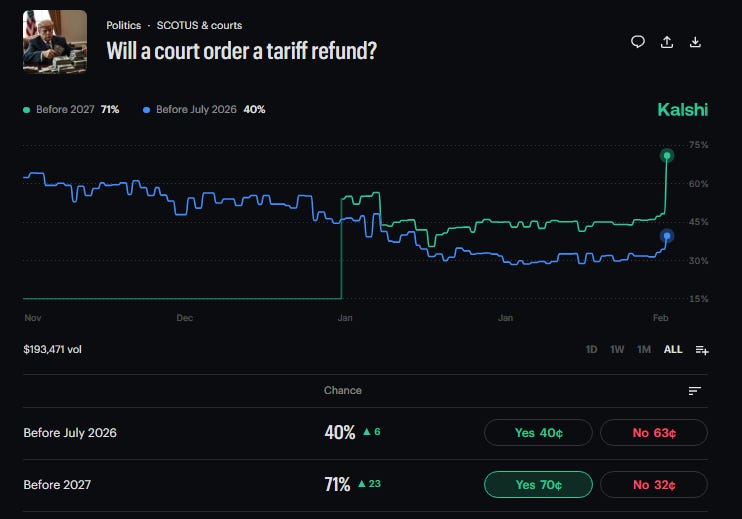

The Supreme Court Rules — and Trump Improvises

The Supreme Court struck down the administration’s global tariff authority, and prediction markets moved immediately.

Justice Kavanaugh, in dissent, captured the practical reality: returning billions of dollars already collected from importers would have “significant consequences for the U.S. Treasury” and the process would likely be a “mess.” He’s right.

The refund mechanics alone introduce a layer of fiscal uncertainty that will take quarters to resolve.

But Trump didn’t blink. Within hours, he held a defiant press conference and outlined a workaround:

A flat 10% global levy within days under Section 122 of the Trade Act of 1974, which grants unilateral authority but caps duties at 150 days.

Existing Section 301 and 232 tariffs (covering Chinese goods, autos, and metals) remain in place.

New trade investigations to be launched that could replace the flat rate with permanent, targeted tariffs before the 150-day window closes.

Auto tariffs of 15–30% under active consideration.

The Supreme Court ruling is constitutionally significant but practically limited. Tariffs aren’t going away. The administration has multiple legal pathways and is clearly willing to cycle through them. For markets, the key variable isn’t whether tariffs continue — it’s the rate uncertainty.

We’ve moved from a regime of high-but-stable tariffs to one of high-and-legally-contested tariffs, which is worse for corporate planning and capex decisions.

The near-term reaction, with stocks rising on the 10% announcement because it was less than the 15% maximum, shows the market is trading the change, not the actual level.

That’s complacency.

If the administration uses the 150-day window to stack new Section 232 investigations and convert temporary duties to permanent ones, the effective rate goes higher, not lower.

Closing the Notebook

It’s late now.

The coffee’s long gone and I’ve got about fifteen browser tabs still open — Fed papers, Yale spreadsheets, Kalshi charts, a half-read Bloomberg terminal article about Section 122 case law that probably doesn’t exist yet.

Here’s where my head is at after a full day of pulling this apart:

The data isn’t ambiguous.

The Richmond Fed warned us.

The New York Fed quantified it.

Yale tracked it in granular detail.

Every credible study arrives at the same destination: tariffs are a domestic tax, the burden falls overwhelmingly on American consumers and businesses, and the promised renaissance in employment and manufacturing hasn’t materialized in any meaningful way.

You can argue about the degree of pass-through — 86% or 94%, 31% or 63% — but the direction is unanimous.

What genuinely unsettles me isn’t the tariff data.

I can adjust for higher costs and shrinking margins. What I can’t predict is the slow weakening of the institutions that provide the data I depend on.

When Hassett calls for Fed economists to be “disciplined” for publishing inconvenient findings, when a president tells a bank to fire its chief economist for not being optimistic enough, and when the Treasury Secretary publicly targets an FX strategist, that’s not just policy disagreement.

That’s a systematic effort to make the cost of honest analysis higher than the cost of staying silent.

And when researchers start self-censoring, not because the data changed but because the personal risk of publishing it is too high, you get a market failure in producing information.

The same government that claims tariffs will improve economic efficiency is actively degrading the efficiency of the information ecosystem that markets depend on. Every investor loses a critical input into the mosaic.

We’re all flying a bit more blind, while those responsible for that blindness are the ones insisting the view has never been clearer.

I’ll keep reading, keep writing, keep putting numbers on things.

That’s the job.

But I’d be lying if I said the atmosphere hasn’t shifted.

Be careful about what you publish these days.

It might be you getting the 3 AM Truth Social treatment next.

Watch who they attack. It’ll tell you exactly what findings they’re most afraid of.

— Riko

Thank you and take care

Great write-up.

I agree and I came to the same conclusions re. the tariffs and USD/fx. Honestly, you do not need a huge "study". It's just logic. Why would you, an exporter, "eat the costs" if a tariff gets put on your goods?

As a vendor or importer you can front-run, a natural behavior of stockpiling so you can enjoy higher margins (massive capital investment though and it can go very wrong); or you can say: c'est la vie - let em have it and increase prices and maybe if you are in a competitive market and need to protect your market share, you eat a bit of the tariffs but will likely to other tricks like reducing quality/sizes depending on your product. That's just me putting my "industrial company" hat on and pulling out my "selling stuff" playbook.

It'll be bad for the currency (devaluation through potentially runaway inflation because of the price hikes through tariffs - you have "more tax receipts" but the deficit piles up in consumer's and industry's books); it'll be bad for GDP (money printing, debt) and it's bad for industry (price fighting, instability, very high policy uncertainty stifle innovation and decisions).

And in regards to the "shoot the messengers" or "dis the scientist":

It's always the same throughout history.

- first they ignore you.

- when it's too evident you were right, they'll try to discredit (ad hominem phase - this is where we are now) - aka "they fight you"

- then you and society lose in most cases, because most of society usually does not back you up until whatever it is you warned them about hits their doorsteps, hard, way later.

- if you're lucky you still see redemption or you live like Diogenes, in a barrel somewhere far away, telling people to get out of your sun

- in extremely rare cases, you'll get retroactively famous and if you're still alive you might even get a medal or something?