The Three Scenarios

On Cipollone’s Milan speech, Fitch’s five-month assumption, and the variable the ECB cannot put in a baseline

Piero Cipollone gave a speech in Milan on Tuesday last week that I have been turning over for seven days.

The venue was the 2026 Sustainable Development Festival.

The audience was not the usual one for an ECB board member — environmental policy people, climate finance people, the sort of room where the words energy transition land softer than they would in Frankfurt.

The press picked up one line.

“The current situation seems to be drifting away from our March baseline projections, which increases the likelihood that we may need to adjust our policy rates.”

Bund 10s lifted four basis points before lunch.

The market read it as a rate-hike signal.

It is a rate-hike signal, and it is also something else.

That is the actual story of last week.

Cipollone laid out the framework, and Fitch revealed why the framework is already obsolete.

Three scenarios, one shape

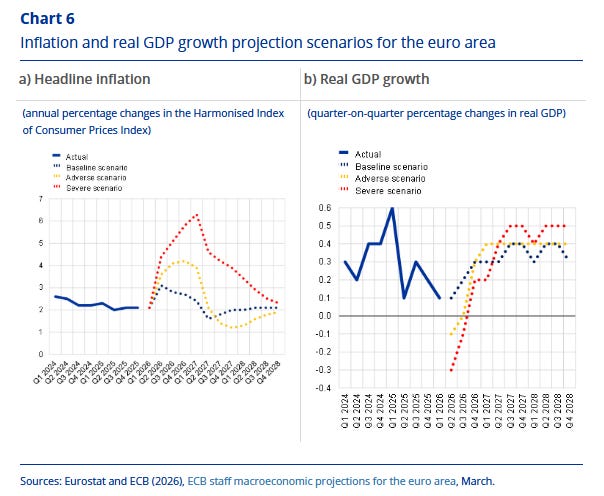

The three scenarios are spelled out cleanly, and it is worth reading them as a unit.

Baseline — published March 2026, with HICP peaking at 3.1% in Q2 2026, decelerating to 2.7% in H2, and returning to target through 2027. Oil and gas prices follow the futures curve, and the Hormuz disruption is treated as a temporary supply shock with a mean-reverting price impact.

Adverse — oil peaks at $119/bbl in Q2 2026 and gas at €87/MWh, both declining thereafter, with cumulative inflation 1.5 percentage points higher than the December projection and cumulative growth 0.8 percentage points lower. Sharper, more persistent, but the variable still mean-reverts — it just takes longer.

Severe — oil peaks at $145/bbl and gas at €106/MWh, both declining at a slower pace, with cumulative inflation 6.3 percentage points higher through 2028.

Read them together and you see what the architecture assumes.

All three scenarios have the same shape — a price spike followed by a return path. The peak height differs. The decline rate differs.

The shock has a beginning, a middle, and an end, and the question for the Governing Council is which of three curves the variable will trace.

The scenarios bound the future by varying intensity, duration, and propagation — the three nouns Cipollone uses repeatedly, and which deserve attention because they describe what is inside the model and therefore what is outside it.

What is inside the model is a price shock.

What is outside the model is a regime change in how the price is determined.

Fitch walked the assumption

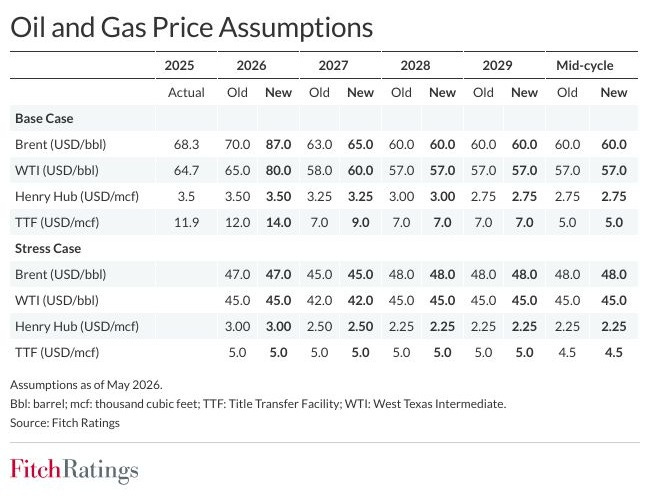

Two days after Cipollone spoke, Fitch published.

The text is dry — The change is not.

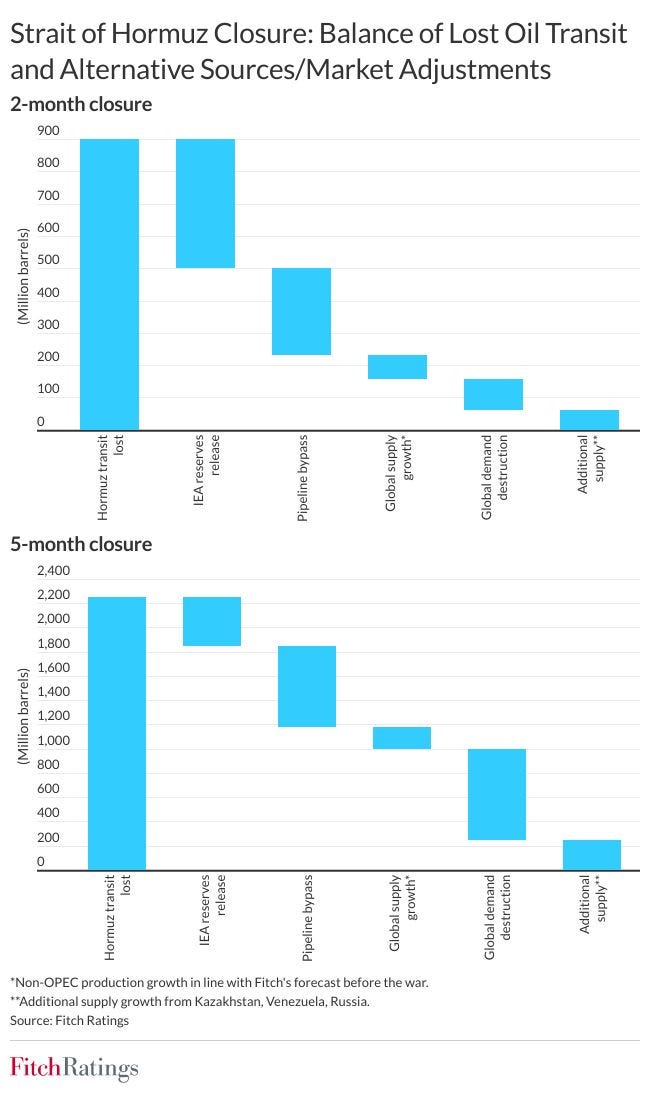

Before this revision, Fitch was working off a “one-to-two month” closure assumption. That is the same window the ECB’s March baseline implicitly priced — short enough that the futures curve does the work, short enough that you can call it a supply shock and look through it.

After the revision, Fitch assumes the strait will “begin reopening around July” and that the closure period will run “about five months.”

The path Fitch now sees is Brent at $100-110/bbl in May through July, then falling to $70/bbl by September.

That September number is not a forecast of de-escalation.

It is the residual price after OPEC produces to maximum capacity, non-OPEC supply growth runs at 3 mmbpd, and oversupply hits the market post-reopening.

The agency assumes 5% of global oil demand needs to be destroyed during the closure window to balance the market — a level Fitch itself calls “possible, albeit severe.”

The institution is no longer arguing about whether the shock is transitory.

It is the duration assumption that makes the price model tractable.

This matters because Cipollone’s adverse scenario is built on the same assumption Fitch has just walked.

The $119 oil peak and €87 gas peak in Q2 2026, declining thereafter — that path requires the closure to behave the way Fitch previously assumed it would.

Once the closure runs five months instead of two, the adverse scenario stops being adverse. It starts being baseline. And severe stops being severe. It starts being adverse.

The ECB updates its scenarios in June. I would be very surprised if the architecture survives intact.

Tuesday’s tape

Yesterday’s tape belongs in the same paragraph as the scenarios, because tapes do not respect architectures.

Brent settled around $107 on Tuesday.

WTI around $99.

TTF gas trading at €44-46/MWh after a 4.7% one-day move higher on Monday.

Aramco’s CEO told the Milken Conference last week the market is losing roughly 100 million barrels of supply per week and that prolonged disruption could push normalisation into next year.

Reports surfaced of the White House weighing a return to military operations.

Netanyahu said the conflict with Iran is “not over.”

Iranian forces fired drones at the UAE. The US sank Iranian small boats in response. Fresh attacks near Qatar.

None of that lines up with a return-to-target inflation path that has Q3 2026 at 2.7% and 2027 at 2.0%.

The tape is pricing tail risk.

The architecture is pricing mean reversion.

The gap between the two is the cost of using scenarios as your decision framework when the underlying variable is not stochastic in the way scenarios assume.

Scenarios are a sound tool for bounding uncertainty around a process whose statistical structure you understand, and a poor tool for pricing political variables that produce binary outcomes.

The Hormuz closure is the second kind — either the ceasefire holds and the strait gradually reopens, in which case Fitch's July assumption stands and we converge to a path between baseline and adverse, or the ceasefire breaks, the US re-enters kinetic operations, and the closure becomes structural, in which case we are above severe with no return trajectory the scenarios contain.

The probability distribution over those two states is a coin flip with a thumb on the scale, and the thumb is in Tehran and Washington, not in Frankfurt.

The architecture shapes the variable

This is where reflexivity walks back into the room.

That communication does work in the real economy.

Firms set prices on the assumption that input costs will decline.

Wage bargainers anchor on the assumption that the spike is temporary.

Treasuries set discretionary spending profiles on the assumption that the deficit impulse is one-off.

Banks tighten credit standards within the bounds of the projected downturn rather than the possible one.

The architecture shapes the variable it is trying to model.

This is the part Cipollone almost gets to. Late in the speech, he says that

"Our dependency on fossil fuels multiplies these effects”, and that "the current energy crisis thus underscores the pressing need to further reduce our reliance on fossil fuels not only because of climate risks but perhaps even more clearly because of energy security risks that are likely to be with us for some time."

That sentence is the entire moral case — decarbonisation as price stability infrastructure, sustainability as the precondition for stability.

But the scenario architecture undercuts that conclusion in the same speech.

If the worst plausible outcome ends with declining energy prices in 2027 and a return to target by 2028, then fiscal authorities have no urgent reason to accept the political cost of accelerating the transition.

The architecture tells them the shock will pass, the moral tells them they should act as if it will not, and both cannot be operative — the architecture wins, because the architecture is what gets quoted in finance ministry memos.

The ECB’s scenarios are not a passive measurement of the inflation outlook.

They are an active input into the political economy of the response, and the response, as a result, is asymmetric to what Cipollone is calling for.

Two hedges, one buried

Cipollone hedges the architecture in two places, and the hedges are worth reading next to each other.

The first hedge is the line that moved the front end —

“The current situation seems to be drifting away from our March baseline projections”

— and it is doing more than signalling a hike. It is saying that the scenario architecture itself, two months after publication, has lost its anchor variable.

The baseline is no longer the central tendency, and that is not normally how baselines work.

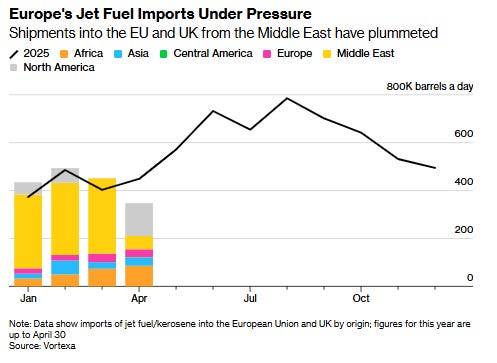

The second hedge is buried later in the speech.

“Europe could start running out of jet fuel and kerosene reserves by the end of May, potentially leading to material restrictions on the activity of several industries akin to those seen during the COVID-19 pandemic.”

That is the most important sentence in the document.

Where Cipollone is right, and where he isn’t

Cipollone is right about decarbonisation, and the structural case is correct.

He is also right that monetary and fiscal responses to supply shocks are costly even when calibrated well, which is a true sentence and a brave one for a central banker to say out loud, and the implication — that the right answer is to remove the dependence, not to respond to the disruption — follows directly.

What he is wrong about is the framework for thinking about how the shock evolves. The scenarios are not three points on a probability distribution — they are three illustrative paths along the same shape, and the shape is the assumption. The shape is mean reversion of a politically determined variable, and that assumption is not in the data — it is in the architecture.

The right framework for the current moment is not three scenarios but two states.

State one: the ceasefire holds, the strait gradually reopens through summer, Fitch’s revised path runs, and we land somewhere between the new baseline and the new adverse.

State two: the ceasefire breaks, the closure becomes structural through year-end, and we are above severe with no return trajectory the model contains.

The probability split is a political variable, and the ECB does not price political variables — it uses scenarios as a substitute, and the substitute is failing.

Three windows

Three windows over the next eight weeks.

Window one. Ceasefire status, day by day — Iran’s response to the one-page memorandum, US naval blockade posture, attacks on UAE/Qatar/Kuwait shipping. The single most important variable for every European asset price is whether the closure runs five months as Fitch now assumes, or eight months, or twelve.

Window two. ECB June projections, where the architecture either updates or it doesn’t. If the new baseline incorporates a five-month closure as the central case and the adverse scenario moves to a structural-closure assumption, the ECB is catching the tape and the policy response becomes legible. If the baseline still assumes a one-to-two month closure with mean reversion, the gap between architecture and reality widens, and the rate path will be revised meeting by meeting in a way markets cannot front-run.

Window three. Jet fuel and kerosene reserves at end-May. Cipollone flagged this as a potential trigger for pandemic-scale industrial restrictions, and if the headline materialises, the inflation expectations channel that has so far held — the line about long-term expectations being "well anchored" — comes under pressure no scenario in the speech describes.

Across all three, the same question.

The architecture assumes the variable mean-reverts, but the variable is not stochastic — it is political. The scenarios will get revised, and the revisions will look like the Fitch update: small in language, large in content.

The institutions catch the tape, they never lead it.

That is what last week was about. Cipollone published the framework, Fitch revised the assumption two days later, and the tape on Tuesday this week told you that even the revised assumption is contingent on a ceasefire the President of the United States describes as being on massive life support.

Thanks, Riko. Your essays are always thought provoking. All of the asset classes I trade, equities (especially), credit, FX, energy and metals seem to underestimate the risk of renewed fighting in the Middle East (with the possibility of more countries involved) and/or the risk that Hormuz remains effectively closed. When all of the markets tell me I'm wrong, I'm probably wrong, at least on timing if not direction. When I'm wrong, I get out. Job one is to protect my capital, especially when I'm wrong. But I really don't think I'm wrong, so I'm looking a "signal" to reposition. Your essay reminds me that "underestimating the risk" has a massive asymmetrical profile.