One Rate, Two Targets

The Reserve Bank lifted the cash rate a quarter-point in May to fight an oil shock the rate cannot reach — and made the 1.3-trillion-dollar escape from oil more expensive in the same motion.

On the fifth of May the Reserve Bank of Australia lifted the cash rate by a quarter of a percentage point, and the sentence that did the real work in the statement was not about jobs or housing but about oil — the risk that the price shock running out of the Strait of Hormuz would seep past the petrol bowser into wages, rents and the expectations that set both.

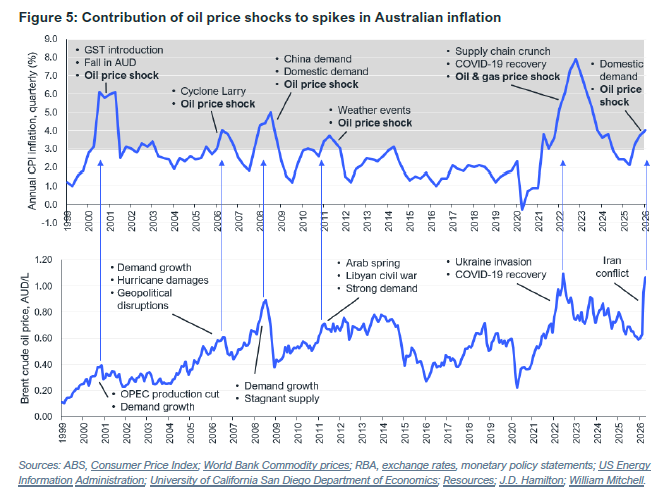

I have spent the past months following that shock through the diesel bill of one importer after another — the Vietnamese pump price that jumped by more than half in a single month, the Bangladeshi input costs that climbed and would not climb back — and the pattern never changes: the molecule sets the price offshore, and the price walks through freight, margins and the consumer index before any central bank lays a hand on it. It is the same pattern, in Australia, behind every inflation spike of this century — six of them, each with an oil shock somewhere in the cause.

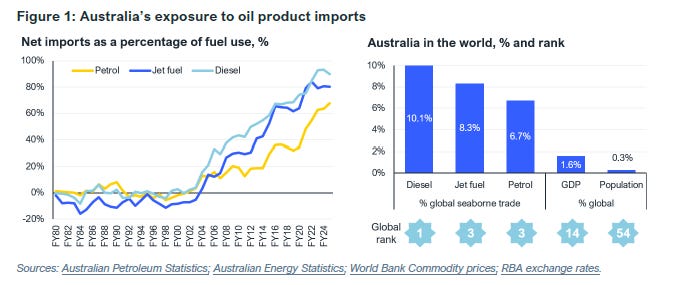

Australia is the wealthy instance of that exposure, and on one measure the most exposed of all. It is the largest importer of seaborne diesel on earth.

I read the May statement twice, looking for the trade-off it did not name.

The hike was not a mistake; it was the correct use of the only instrument the Bank holds.

That is exactly the problem.

IEEFA has set the whole mechanism down across thirty pages, and the thing underneath the data is reflexive to its core: the tool reached for to contain this year’s oil-driven inflation raises the price of the one asset that would stop next year’s oil shock from becoming inflation at all.

The target the rate can see

The Reserve Bank works with three tools, and all three point the same way — inward, at domestic demand. It states an inflation target of two to three per cent to anchor expectations; it sets the cash rate, the overnight price of money between banks, which travels out into mortgages, business credit and the currency; and it offers forward guidance on the rate’s path before the rate itself moves.

The transmission is textbook.

A higher cash rate makes borrowing dearer, cools investment and asset prices, drains income from mortgaged households, and lifts the exchange rate, dragging down import prices. Every one of those channels runs through a domestic decision — someone borrows less, builds less, buys less.

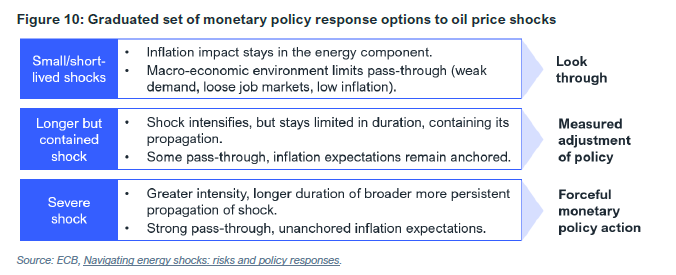

When the shock is an oil shock, the Bank does not pretend the rate can reach the price; it fights the spillover instead, on a sliding scale — look through a small move, adjust for a contained one, act forcefully only when a severe shock threatens to unanchor expectations.

May was the Bank moving up that scale, and the trigger sat in the price the household sees first: in March, transport costs alone added a full percentage point to the consumer index and pushed inflation past four per cent.

That is the target the instrument was built to hit — broad-based, demand-side inflation and the expectations that feed it.

The difficulty is that the inflation now in front of the Bank was not made by the demand it can see.

The price that pushed inflation past four per cent was not struck in a domestic auction room or a wage round. It was struck in a strait twenty-one nautical miles wide, and no setting of the cash rate reaches it.

The price it cannot touch

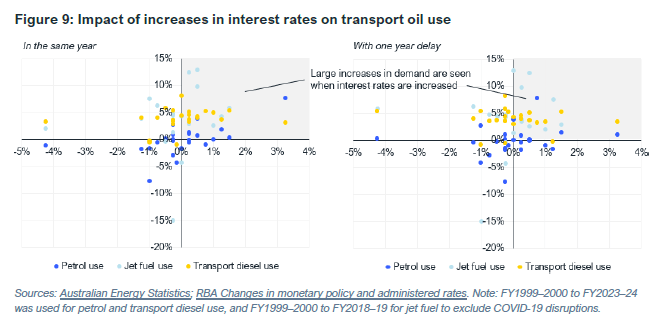

Oil demand does not bend to price the way the textbook diagram promises, and it has not for fifty years. The Bank’s own research puts the demand contraction after a ten per cent price rise at as little as one to two per cent — close enough to inelastic that, for the purpose of policy, the curve is a wall.

What I keep returning to is where the report stops citing the literature and tests the Australian case directly: demand for petrol, jet fuel and transport diesel shows no response to the crude price, in the same year or lagged a year, while transport diesel simply grows above three per cent a year.

The rate cannot reach the demand; the demand cannot reach the price.

Read that the way a risk officer reads a concentration limit.

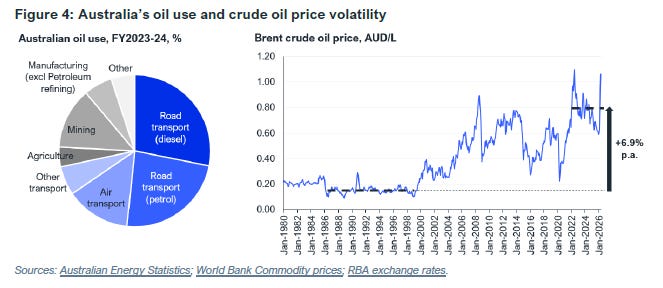

And the buffer behind it is the thinnest in the developed world: forty-five days of net imports in stock, the lowest of any International Energy Agency member and the only one beneath the agency’s ninety-day floor, against a net-importer average of one hundred and forty-one. That price has climbed about seven per cent a year in Australian dollars since 2000, more than double the consumer index, and grown more volatile with every Gulf flare-up.

The cure it prices out

There is a way out of the trap, and the report names it without hedging: electrify transport. Transport burns close to three-quarters of Australia’s oil and is the largest route by which oil reaches inflation — through household fuel bills, through the diesel in the cost of goods, and through the visible pump price that moves expectations beyond its budget share.

Swap the imported molecule for a domestically generated electron and the channel is cut at the source.

This is the asset that ends the exposure — and the most rate-sensitive asset in the entire transition.

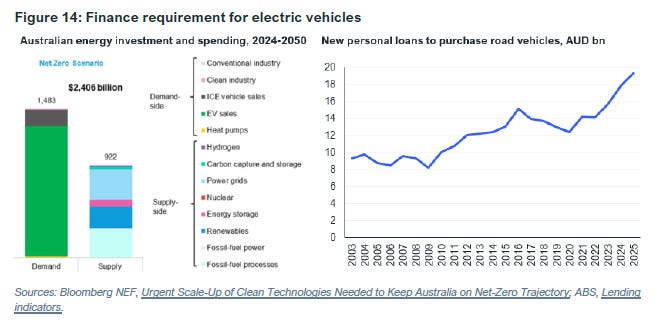

Electric vehicles are the single largest line in Australia’s net-zero bill — 1.3 trillion Australian dollars to 2050 on Bloomberg New Energy Finance’s estimate, larger than the whole supply side of renewables, storage, grids and hydrogen combined.

Capital-intensive, debt-financed assets are precisely the ones a rate rise punishes hardest. Wood Mackenzie has drawn the asymmetry cleanly: higher borrowing costs fall heavily on low-carbon energy, where debt is a large slice of the capital structure and capital expenditure is most of the spend, and lightly on oil and gas, which carries far less exposure to debt.

Read the May decision the way a freight operator’s financing desk reads it.

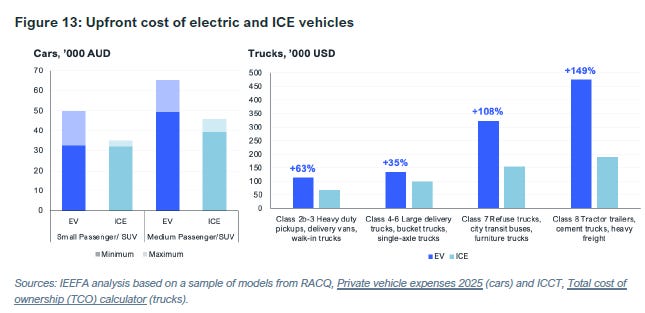

The desk is weighing an electric prime mover against a diesel one; the electric truck already carries a purchase premium that runs into triple digits in the heaviest class; and the quarter-point the Bank has just added to the price of money has widened the lifetime gap by tens of thousands of dollars before the operator turns a wheel.

The same instrument, in the same motion, has fought the demand-side spillover of the oil shock and raised the price of the asset that would end the oil dependence the shock feeds on.

One knob, two targets — and the knob is wired so that turning it toward the first turns it away from the second.

The hike that preserves the dependence

Here the loop closes, and it closes cleanly enough to name each turn.

Begin with the belief: a rate rise in the teeth of oil-driven inflation is stabilising, the orthodox and correct move, the Bank doing its job.

The belief shapes behaviour — the Bank lifts the cash rate to contain the spillover, citing the danger that expectations slip their anchor, and the cost of capital rises across the economy in step.

The behaviour alters the fundamental — the dearer capital slows the one investment that would sever the oil-to-inflation channel, the electric fleet, so the freight that moves the country stays on imported diesel and the dependence is preserved rather than retired.

And the altered fundamental feeds back on the belief, confirming it for a cycle and dismantling it over the next: because the dependence is intact, the next disruption out of the Gulf reaches Australian inflation exactly as hard as this one did, which summons the next hike, which slows the escape again.

This is the act of participation at the centre of Kardamow’s frame — the intervention meant to read and contain a condition quietly rewriting the condition it was reading.

The fire-fighting feeds the fire.

The inflection — the point where a self-reinforcing tool turns self-defeating — is invisible inside any single decision.

The reflexivity lives in the accumulation — a run of individually correct rate decisions, each fighting this year’s symptom by entrenching the structure that guarantees next year’s, until the instrument’s medium-term effect inverts its short-term intent.

The report supplies the back half the Bank has not priced: that the same tightening raises the price of the only durable defence. This is the shape I keep finding when I pull on an energy thread — the remedy on the wrong side of the very tool meant to apply it.

Jan Tinbergen wrote the rule that explains why.

Two targets, two instruments

The Reserve Bank has one instrument.

In an oil-shock world it has two targets — cool the demand-side spillover now, cheapen the supply-side escape from oil — that pull in opposite directions through the single tool it owns. One instrument cannot satisfy two targets in conflict; the arithmetic forbids it, and the May hike is what the forbidden looks like in practice.

The Bank’s objection to the obvious fix deserves its strong form.

A discounted facility for clean lending, it would say, works against the tightening — it loosens credit in one corner just as policy tries to drain it, slowing inflation’s return to target and, on the worst reading, delaying the transition it means to help.

Take it seriously.

Then resolve it on the mechanism, the way the report does: the second instrument need not touch the first instrument’s target.

A refinancing facility priced off the central bank’s own balance sheet rather than off the cash rate can cheapen electric-vehicle credit without warming or cooling domestic demand — and because the vehicles are overwhelmingly imported, the facility shifts the composition of what households buy rather than adding to domestic activity, the channel the cash rate polices. It makes the electric truck and the diesel truck cost about the same to own — no cheaper, no windfall, the gap simply closed.

It works the other target.

It does not contest the first.

None of this is hypothetical; the instruments exist and run today — the bank is being asked to redirect a tool, not invent one.

China’s central bank refinances sixty per cent of qualifying clean-energy loans at one and three-quarter per cent through its Carbon Emission Reduction Facility, extended to at least 2027 and credited with over a hundred billion US dollars of green lending.

The Reserve Bank itself ran a term funding facility at a tenth of a per cent through the pandemic, with one hundred and eighty-eight billion dollars outstanding when it closed.

The New Economics Foundation has proposed exactly this design for the Bank of England; the French National Assembly has asked the ECB to study green dual rates.

Two instruments, two targets, each aimed where it can land.

The rate inside the shock

Now that the whole chain is on the table, the sharpest thing in it is the one the argument hid until the loop closed: the cash rate is not a dampener sitting outside the oil-price transmission and trying to absorb it — it has become a link inside it. By raising the price of the cure, the instrument meant to interrupt the channel from the Strait to the consumer index has joined it, one more stage by which the next Gulf disruption reaches Australian inflation.

I do not think the May hike was wrong.

I think the belief underneath it was — that a single cash rate is equal to an inflation imported in molecules a domestic instrument cannot touch.

The Bank has been handed an impossible brief: to hold price stability against a price set offshore, and to fund the only lasting defence against that price, both with the same hand.

The line I would put in front of the Board is short.

An economy whose price shocks are imported needs a second instrument aimed at the imports’ replacement, and monetary policy as currently equipped does not have one.

Walk the cost to where it lands.

The freight operator runs the electric prime mover against the diesel one, the financing desk prices it off a cost of capital the May decision just lifted, the order does not convert, the depot keeps buying diesel — and across a fleet that turns over slowly, the national diesel import bill stays where it is.

The price of that, for the energy market itself, is not only the pump.

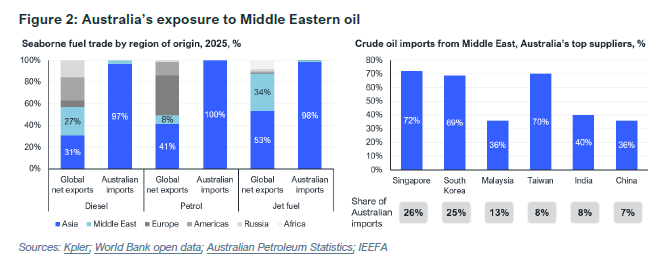

It is the structural diesel-to-Brent premium that opened in this crisis — the spread that ran past a hundred dollars a barrel because the Gulf supplies both the diesel and the sour crude grades the Asian refineries Australia leans on are built to run.

A country that does not electrify keeps that spread on its import account as a standing line, and keeps the option value of the Hormuz chokepoint sitting, unhedged, on a national balance sheet that has chosen — by leaving the cash rate to do everything — to stay long oil. The second instrument is the hedge against that position. Its absence is the position.

And the timing sharpens the point rather than softening it: the shock that set all this off is already easing — a Hormuz understanding signed between Washington and Tehran, the diesel and crude benchmarks down sharply from their June highs — and yet nothing it exposed has shifted, because the next disruption out of the Gulf still meets the same ninety-per-cent import dependence, the same thin reserve and the same single instrument wired the same way.

The fix was never for this shock; it is for the next one, already pencilled in.

So here is what I am watching, on a clock already running — and the first marker has already fired.

The fuel-excise cut announced on the thirtieth of March was a three-month measure due to lapse on the thirtieth of June, and rather than let it expire Canberra extended it into August at half the rate — which is the admission, written in fiscal form, that the monetary tool has run out of road, the government now paying close to three billion dollars in forgone revenue on the first tranche alone to hold down a bowser the cash rate cannot touch. The patch renewed is the tell.

Then the next Reserve Bank statement, for any language on a facility or a dual rate — its first appearance is the signal the Bank has accepted it carries two targets and gone looking for the second tool.

Then the electric share of new heavy-vehicle sales, under one per cent through May, the dial the whole thesis must move off its floor. And the diesel-to-Brent spread, the live read on the exposure itself.

The rate the Bank raised to fight the oil is the rate that keeps it